What Is Home Equity Release in Dubai and How Can You Unlock It?

19/06/2026

|9 min read

Unlock the value of your property with home equity release in Dubai. Get clear insights into eligibility, financing options, and costs.

What Is Home Equity Release in Dubai and How Can You Unlock It?

Dubai's property market has delivered remarkable value growth over the past several years, and for many homeowners, that growth has quietly built up a significant financial resource sitting unused within the walls of their home. The challenge is that most people do not know this resource exists, or they assume that accessing it means selling up and moving on. Neither is true.

Home equity release allows you to tap into the value your property has accumulated without selling it, without moving out, and without disrupting your life. In the UAE, it is most commonly used to fund meaningful home improvements or to finance the purchase of a second property.

For homeowners who have seen their property values rise and their mortgage balances fall, it represents one of the most practical and cost-efficient ways to put that growth to work.

This guide explains what home equity release is, how the process works in the UAE, and how to navigate it with the right support.

What Is Home Equity Release?

Home equity release is a financial arrangement that allows property owners to access the value built up in their home without having to sell or vacate it. It turns a portion of your property's worth into usable capital, while you continue to live in or own the property as normal.

To understand equity release, you first need to understand what home equity actually means. Your equity is the difference between what your property is currently worth on the open market and the amount you still owe on any mortgage or loan secured against it.

For example:

- Current market value of your property: AED 2,000,000

- Remaining mortgage balance: AED 500,000

- Your equity: AED 1,500,000

Your equity builds over time in two ways. First, every mortgage payment you make reduces what you owe, incrementally increasing your ownership stake in the asset. Second, when the property's market value rises, your equity rises proportionally even if your outstanding balance has not changed.

In a market like Dubai, where property appreciation has been consistent and significant in recent years, many homeowners find their equity has grown substantially without them having done anything other than maintain their property and continue making repayments.

Equity release converts a portion of that accumulated value into accessible funds. The key distinction from selling is that you retain your ownership and your home. The funds can be structured as a lump sum or, depending on the product type and lender, as a line of credit that can be drawn down over time.

How Does Home Equity Release Work?

Home improvements represent the most common use of equity release in the UAE. Whether you are modernizing a kitchen, extending a living space, adding a pool, or comprehensively refurbishing an older apartment, using the equity in your home to fund the work is often more cost-efficient than a personal loan and more practical than depleting savings that might be needed elsewhere.

Here is how to approach it:

1. Get an Updated Property Valuation

Before you can calculate what is available to release, you need to know what your property is currently worth. Market values in Dubai shift with supply, demand, and area-level dynamics, and your home today may be worth significantly more than when you purchased it.

Prosper's owner dashboard gives landlords and homeowners a live view of recent comparable transactions in their building and immediate area, giving you a grounded, current picture of where your property sits in the market before you approach any lender.

This is not a substitute for the lender's formal valuation, but it ensures you enter that process with accurate expectations rather than assumptions.

2. Calculate Your Available Equity

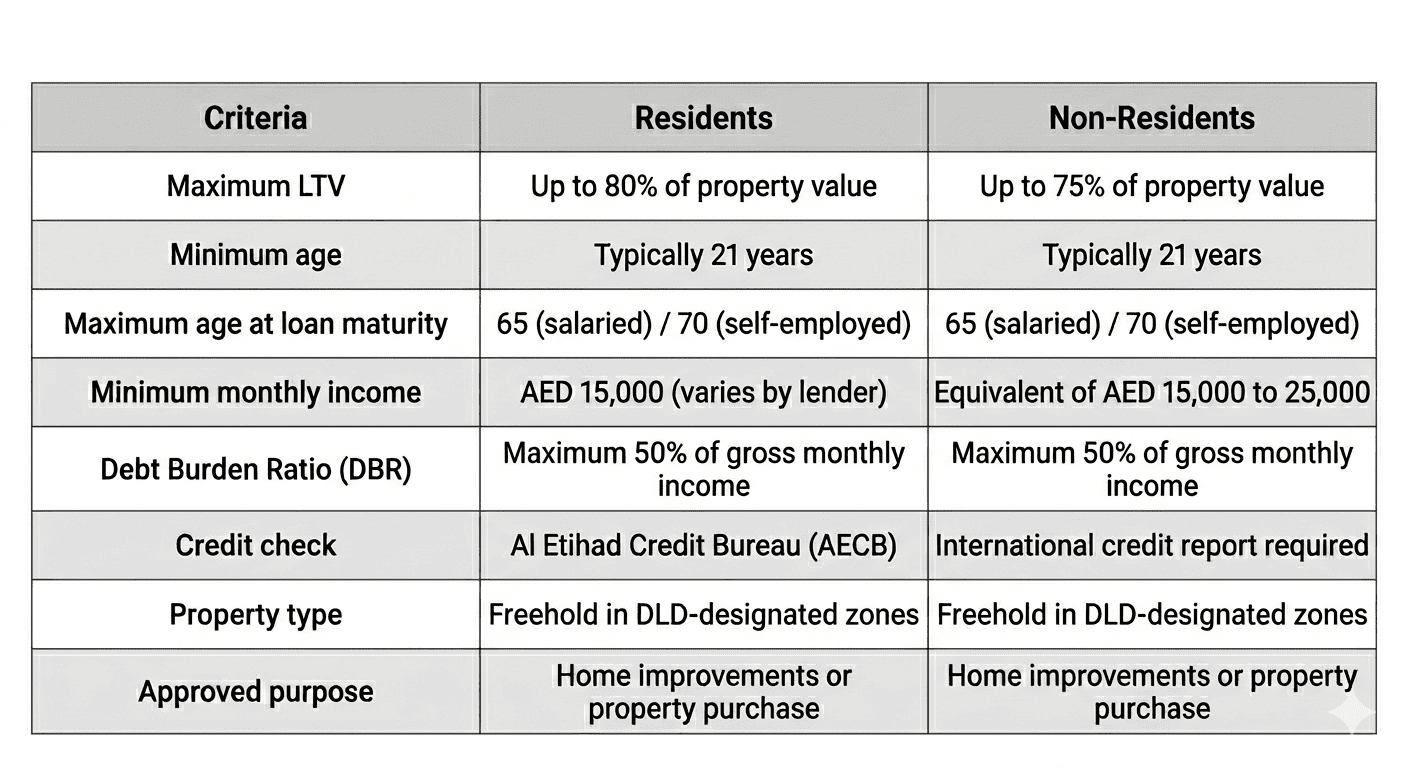

With a current market value in hand, calculate your equity by subtracting your remaining mortgage balance. Then apply the relevant LTV cap for your residency status (80% for residents, 75% for non-residents) to determine the maximum total secured borrowing available. Deducting your outstanding mortgage from that figure gives you the ceiling on what you can release.

Keep in mind that lenders also assess affordability, so the maximum available equity and the amount you are approved to release may differ depending on your income and existing debt position.

3. Connect With My Mortgage

This is the most important step in the process. Equity release products vary significantly across UAE lenders in their rates, terms, LTV allowances, and flexibility. Approaching a single bank directly means you see only one offer, with no ability to benchmark it against the broader market.

Prosper connects homeowners directly to My Mortgage, its renowned UAE mortgage partner. My Mortgage's advisors work with the full panel of UAE lenders offering equity release products and can identify the most competitive structure available for your specific profile, whether that is a straight remortgage with equity, a buyout plus equity arrangement, or a line of credit linked to your property.

My Mortgage also handles the full application process on your behalf, including documentation preparation, lender submission, and coordination with the bank through to approval. Their advisors know which lenders are most receptive to renovation-purpose applications and which structures are most likely to be approved based on your income, property type, and LTV position.

4. Choose Your Loan Structure

The most common equity release structures for home improvement in the UAE are:

- Lump sum remortgage: Your existing mortgage is refinanced and the additional equity is released as a single lump sum at the point of completion. This is the simplest and most common structure for renovation projects with a defined scope and budget.

- Buyout plus equity: Where an existing mortgage from another bank is bought out and a new, larger facility is established with the releasing bank. This can also allow the homeowner to access a more competitive interest rate on the remaining mortgage balance at the same time as releasing equity.

- Line of credit (available from select lenders): A flexible facility where equity is made available to draw down as needed, rather than as a single upfront payment. This suits renovation projects that are phased over time and where costs will emerge progressively.

My Mortgage will help you determine which structure fits your renovation timeline, your budget phasing, and your financial profile.

5. Submit Your Application

Once you have selected a product and lender, My Mortgage coordinates the full application submission. This includes the property valuation appointment, all required documentation (passport and Emirates ID, income evidence, bank statements, existing mortgage statement, and details of the renovation work planned), and ongoing liaison with the lender through the credit and legal assessment stages.

You are kept informed throughout, and My Mortgage handles any requests for additional information from the bank to prevent delays.

6. Release Your Funds and Plan Your Renovation

On approval, funds are transferred as agreed. From this point, Prosper's platform continues to work for you as a homeowner. Your owner dashboard tracks your property's ongoing market value and ROI performance, which is particularly valuable once improvements are complete and you want to understand how the renovation has affected the asset's overall position.

Your dedicated Relationship Manager is available for any questions about the property's performance post-renovation, refinancing reviews when your rate period approaches its end, and future equity release options as your property continues to appreciate.

Eligibility Criteria for Equity Release in the UAE

Not every homeowner will qualify for equity release, and understanding the criteria before approaching a lender saves time and prevents unnecessary credit inquiries. Here is a breakdown of the key requirements.

Core Eligibility Requirements

Property Requirements

The property itself must meet a number of conditions before a lender will approve an equity release application:

- Sufficient equity built up: The property must have enough equity above the existing mortgage balance to make the release viable after applying the LTV cap

- Freehold ownership: Leasehold properties face significantly more restrictions, and some lenders will not advance equity release against leasehold titles where fewer than a specified number of years remain

- Clean title: The property must be free of legal disputes, encumbrances, or unresolved issues that would prevent a clear DLD mortgage registration

- Acceptable property condition: Lenders conduct a valuation to confirm the property is in a condition that supports the assessed market value. Properties with significant unresolved structural issues may attract a lower valuation or be declined

- Dubai freehold zones only: Properties outside DLD-designated freehold areas or in non-freehold communities are not eligible for UAE bank equity release products

Financial Requirements

- Debt Burden Ratio (DBR): Total repayments must stay within 50% of gross monthly income.

- Income Documentation: Applicants must provide income proof based on employment or residency status.

- Credit History: Clean credit records are required; defaults or missed payments may affect approval.

- Purpose Restrictions: Funds can only be used for renovations or purchasing another property.

5 Benefits of Home Equity Release in the UAE

1. Access Capital Without Selling Your Property

The most immediate benefit is access to a substantial amount of capital without the disruption, cost, and emotional challenge of selling your home. You retain your address, your community, and your asset while deploying its value toward a productive purpose.

2. Lower Interest Rates Than Personal Finance

Since equity release is secured against the property, lenders charge significantly lower interest rates than they would for unsecured personal loans. In a market where current mortgage rates sit in the 3.9% to 4.5% range, the cost of equity release borrowing is materially lower than the rates applied to personal or business loans, which typically range from 6% to 15% or higher.

3. Funds Are Tax-Free in the UAE

The UAE imposes no income tax, capital gains tax, or property tax, which means the funds released from your equity are entirely free of tax liability. Every dirham accessed is yours to use without any reduction from taxation.

4. Increases the Value of the Underlying Asset

When equity release is used specifically for home improvements, a well-planned renovation can increase the market value of the property by more than the cost of the work undertaken. This means the net effect on your equity can be positive even after accounting for the additional loan balance, particularly in a rising market.

5. Flexible Use for Property Growth

In the UAE, equity release supports two of the most financially sound purposes available to a property owner: enhancing an existing asset's value and using capital to acquire a further income-generating investment. Both uses can compound your long-term wealth position rather than simply spending down an asset.

Drawbacks of Equity Release to Consider

1. Reduction in Inheritance

Releasing equity increases the outstanding loan balance secured against your property. When the property is eventually sold, a larger portion of the proceeds goes toward repaying that balance, reducing what passes to your heirs. If leaving a specific amount to family members is a priority, this needs to be factored into your planning.

2. Interest Accumulation Over Time

Some equity release structures, particularly lifetime mortgages and reverse mortgages, do not require ongoing monthly interest payments. Instead, interest accumulates and is added to the loan balance. Over long periods, this compounding effect can substantially increase the total amount owed. Understanding the long-term cost of the product you select is essential before committing.

3. Market Value Risk

Equity release is calculated as a percentage of your property's current value. If property values decline after you release equity, your remaining equity can compress significantly. While many products include protections limiting the debt to the eventual sale proceeds, a falling market can still reduce the financial flexibility available to you in the future.

4. Strict Eligibility and Purpose Restrictions

UAE Central Bank regulations and lender policies mean equity release is not universally available. Lenders assess age, income, property value, existing debt, and the stated purpose of the release. In the UAE, the purpose restriction to home improvements or property purchase rules out several use cases that would be acceptable in other markets.

Applications are assessed against affordability thresholds and all major lenders require documentation confirming the renovation or purchase purpose.

5. Impact on Future Borrowing

Adding an equity release facility to your existing mortgage increases your overall debt-to-value ratio. This can affect your eligibility for future borrowing if your circumstances change, and it reduces the headroom you have before reaching the maximum LTV limit set by the Central Bank.

Streamline Your Home Equity Release In Dubai With Prosper

Home equity release in the UAE is a genuinely practical financial tool for homeowners who have built meaningful value in their property and want to use it productively without selling. Whether the goal is a comprehensive renovation that enhances the asset's value or the acquisition of a second property that expands an investment portfolio, the equity in your home can fund either goal at a cost that most other borrowing options cannot match.

Getting it right requires accurate market data, expert lender comparison, and a structured application process.

Whether your goal is a renovation that adds direct value to your asset or a second property acquisition that grows your portfolio, Prosper and My Mortgage ensure your equity release is structured correctly, efficiently, and in your best financial interest from day one.

Download Prosper today to simplify your home equity release in Dubai.