Why Should You Use A Mortgage When Buying Property In Dubai

25/04/2026

|5 min read

Mortgages in Dubai give you several benefits like a free bank account and maximum rental ROI. Explore these benefits to streamline your property journey.

Why Should You Use A Mortgage When Buying Property In Dubai

Most buyers in Dubai assume that paying cash for a property is the smarter, safer choice, with no bank, no EMI, no monthly obligation. However, this assumption, while intuitively appealing, overlooks some of the most powerful advantages that a mortgage unlocks.

Used correctly, a mortgage does not just help you buy a property; it helps you buy it better, earn more from it, and keep more capital free to do even more with.

The Dubai mortgage market is one of the most competitive and investor-friendly in the world, with rates that often sit well below the rental yields the city delivers. That gap is the engine that makes leveraged property investment in Dubai one of the most efficient strategies available to both residents and international buyers.

In this blog, we break down every advantage of buying with a mortgage in Dubai, what to consider when applying, and exactly what eligibility looks like for residents and non-residents alike.

5+ Benefits Of Buying Property In Dubai With A Mortgage

1. Lower Upfront Capital To Enter the Market Sooner

The single most immediate advantage of a mortgage is that it dramatically reduces the cash you need to commit at the point of purchase. Instead of waiting years to accumulate the full property value, you can enter the Dubai market with a fraction of that capital and start building equity and earning rental income from day one.

For a resident buyer, a down payment of as little as 20% is required to purchase a qualifying property. For a non-resident, 40% down is the standard threshold. In both cases, you are entering ownership of a full-value asset while keeping the majority of your capital free, deployed elsewhere, earning returns, or available for a second purchase.

A mortgage lowers the barrier to entry. It means you don't have to wait until you have the full property value saved. You can start building your position in Dubai's market today, with the capital you already have.

2. Higher Return on Investment Through Leverage

This is the most financially significant advantage, and it works in two distinct ways.

A. Capital Appreciation ROI

Consider a straightforward comparison. You purchase a property for AED 1 million in cash and sell it for AED 1.5 million. Your profit is AED 500,000; a 50% return.

Now the same property purchased with a mortgage, with AED 400,000 of your own capital. You sell for the same AED 1.5 million. Your profit is still AED 500,000, but now measured against AED 400,000 invested. Your percentage return is significantly higher.

The property's appreciation stays the same. The only thing that changes is how much of your own money was at work.

B. Rental ROI

The rent a tenant pays is determined by the property, not by whether you bought it with cash or a mortgage. What changes is the equity base against which that rent is measured. A cash buyer ties up the full purchase price. A mortgage buyer ties up only their down payment and earns the same rent on a smaller equity investment, a meaningfully higher rental ROI from the same asset.

3. Rental Income Can Fully Service Your Mortgage — With Surplus

In many property markets globally, landlords regularly have to top up their mortgage EMI from their own pocket. Dubai is different. The combination of strong rental yields and competitive mortgage rates means that in many cases, the tenant effectively pays the mortgage for you.

Dubai's net rental yields typically average around 5%, while mortgage rates currently sit in the 3.9–4% range during the fixed tenure, subject to prevailing variable rates once that period ends.

When your fixed rate tenure is over, Prosper assesses and keeps scouting for the best market rates to help you secure the lowest going rate at the time if your variable is high.

That spread is meaningful; rent comes in above the cost of financing. With an LTV of 60% or below and a tenure above 15 years, rental income in most well-located Dubai properties will cover the EMI plus service charges and still leave a cash surplus.

After your initial down payment, you are not continuously injecting capital. The property sustains itself, and in many cases generates cash in hand, while simultaneously building equity from principal repayment. No other investment class in Dubai offers this combination as reliably.

4. Free Bank Account For With a Mortgage

This is one of the most underappreciated practical benefits, particularly for international investors. Opening a personal bank account in the UAE as a non-resident is notoriously difficult. Most banks require large minimum balances or investment in the bank's own products.

The mortgage route bypasses this entirely. When you take a mortgage from a UAE bank, you are engaging with the asset division; the part of the bank that wants to lend. Because the bank has a vested interest in the relationship, it is significantly more willing to open a linked account for the borrower.

What this account provides: zero minimum balance, online banking access, a debit card, and a UAE-based account into which rental income can flow and from which the EMI can be auto-deducted.

For overseas investors, this creates an entirely self-contained financial loop: rent flows in, mortgage is serviced, surplus sits in the account, and the investor monitors everything remotely. No third-party remittance requirements, no currency conversion delays. The mortgage effectively creates a UAE financial infrastructure for investors who would otherwise struggle to access one.

5. Independent Valuation and Due Diligence Provided

When a buyer pays cash, they typically rely on the agent or seller to assess whether the price is fair. A mortgage removes this asymmetry by introducing a bank-appointed independent evaluator who assesses the property's true market value before any funds are released. The bank will only lend against the lower of the purchase price or the independent valuation.

Some buyers include a clause in the MOU allowing them to renegotiate or withdraw if the bank valuation comes in below the agreed purchase price, turning the valuation into structured price protection that costs a fraction of the transaction value.

The bank's credit and legal review becomes an added safeguard. Essentially a free legal and due diligence service layered over the transaction, particularly valuable when buying from a distance or in an uncertain market.

Even buyers who can afford to pay cash sometimes choose a partial mortgage specifically for this reason. The bank checks the documentation, confirms the title is clean, and verifies the asset is mortgageable, catching problems that independent buyer research can miss.

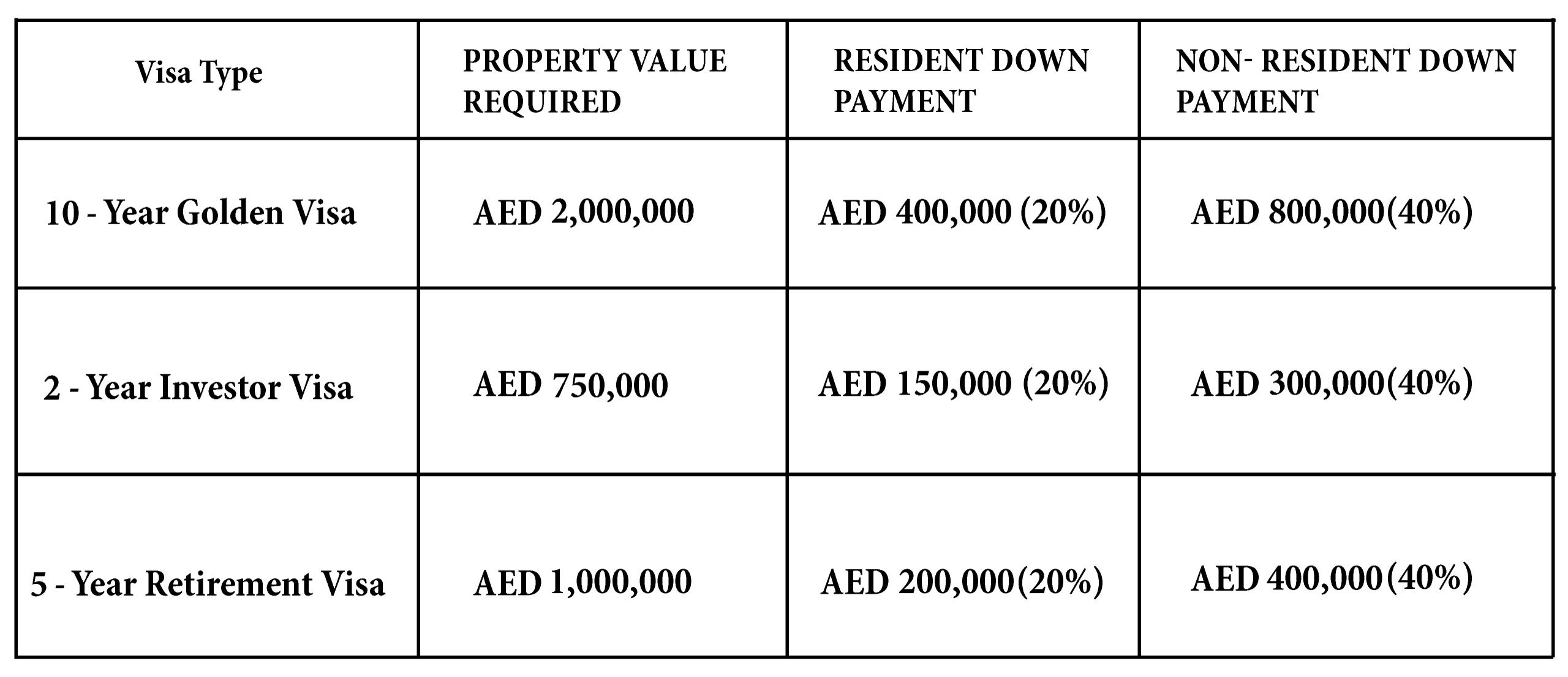

6. Lower Investment To Qualify For a Property Visa

Dubai's property-linked residency visas are well known in principle but underutilized in practice. What fewer buyers realize is that a mortgage dramatically lowers the actual cash required to qualify:

Prosper's mortgage experts can help you structure a qualifying purchase at the most efficient entry point.

A resident buyer can qualify for the 10-year Golden Visa with as little as AED 400,000 of their own cash; the bank finances the remainder. The visa is renewable for as long as the property is owned and is tied to ownership rather than employer sponsorship, meaning losing a job does not affect your residency status.

What to Consider When Applying for a Mortgage in Dubai?

When applying for a mortgage in Dubai, consider your eligibility (income, employment stability, and residency status), the required down payment (20% for residents, and 40% for non-residents), and additional costs like fees, insurance, and registration.

It’s also important to compare interest rates (fixed vs. variable), understand loan terms, and ensure your monthly repayments fit comfortably within your budget.

- Loan-to-Value (LTV) ratio: For residents, maximum 80% on properties up to AED 5M. For non-residents, 60%. Your LTV determines how much financing you can access and what your effective down payment needs to be.

- Interest rate type: Fixed-rate mortgages offer payment certainty for an initial period (typically 1–5 years) before reverting to variable. In the current environment, fixed-rate periods are popular for the predictability they provide.

- Mortgage tenure: Longer tenures reduce your monthly EMI, improving the likelihood that rental income covers repayments. At 60% LTV and tenure above 15 years, rental income in most well-located Dubai properties should service the full EMI.

- Property type and eligibility: Not all properties are mortgageable. Freehold properties in designated zones are generally eligible. Always confirm mortgageability before committing to a property.

- Pre-approval first, property second: Mortgage pre-approval gives you a confirmed borrowing limit before your search begins — allowing you to negotiate from certainty and move fast in a competitive market.

- Additional transaction costs: Budget for the 4% DLD transfer fee, 0.25% mortgage registration fee, valuation fee, and agent commission (typically 2%), approximately 6–7% on top of the purchase price.

- Early settlement fees: Capped by UAE regulations at 1% of outstanding balance (maximum AED 10,000). Factor this into your exit modelling if you plan to sell or refinance within a few years.

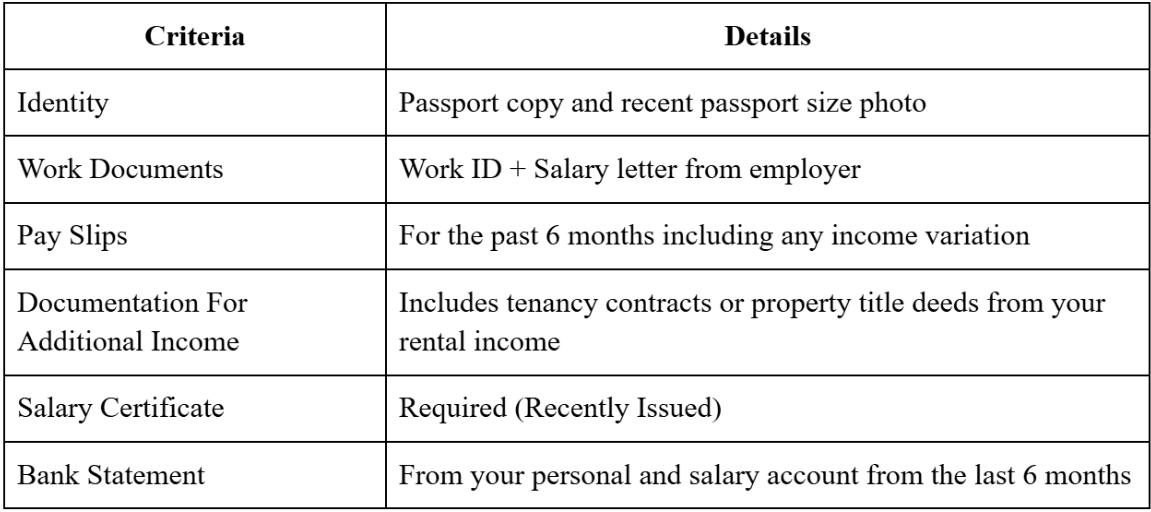

Mortgage Eligibility For Non-Residents

Here is the eligibility criteria for non-residents of Dubai to avail of a mortgage:

Streamline Mortgages In Dubai With Prosper

Dubai's mortgage market is uniquely positioned to make all of this work. With rates sitting below typical rental yields and a regulatory framework that protects buyers at every stage, the leveraged property investor in Dubai has a structural advantage over the all-cash buyer, not just in returns, but in flexibility, risk management, and long-term wealth building.

Prosper’s renowned mortgage partner, My Mortgage, helps you get mortgages at the lowest interest rates and streamline your mortgage journey. Assistance is provided to ensure you make an informed decision.

Download Prosper today to simplify mortgages in Dubai’s real estate market.