Rent-To-Own Properties In Dubai: A Complete Guide

06/01/2026

|11 min read

Unlock home ownership in Dubai with our complete guide to rent-to-own properties in Dubai. Understand eligibility, the application process, and key legal tips.

Rent-To-Own Properties In Dubai: A Complete Guide

Renting in Dubai often feels like the only practical choice for many residents. Monthly payments provide flexibility and a place to live, yet they rarely contribute to long-term financial security.

As property ownership becomes more accessible, many renters are beginning to reconsider how those payments could serve a larger purpose.

Instead of paying rent with no lasting return, this approach allows tenants to direct their monthly payments toward eventually owning the property they live in. Over time, part of what would have been rent can contribute to the purchase of the home itself.

For residents who want a path toward ownership without the immediate commitment of a traditional mortgage, rent-to-own properties in Dubai present a practical middle ground.

This guide explains how the process works, who it suits best, and how renters can use it to move closer to owning a home in one of the world’s most dynamic property markets.

How to move from Renting To Owning a Property In Dubai?

Transitioning from renter to property owner in Dubai is a structured, nine-step process — from assessing your finances and securing mortgage pre-approval, to signing the MOU, transferring ownership at the DLD, and receiving your title deed.

Let’s understand this in detail:

1. Assess Your Finances

Before anything else, know your numbers. Expats need a minimum monthly income of around AED 15,000 to qualify for a mortgage, and considering the property value is below AED 5 million, the minimum down payment is 20% for your first property followed by 40% for your second.

Beyond the down payment, budget for additional costs like DLD registration fees, agency commissions, and property inspection fees. These can add roughly 5–7% to the total purchase price.

For tenants registered on Prosper, your dashboard shows your full rental history, cheque details, and property-specific financials. The platform analyzes your financial profile and rental history to identify personalized financing options, so by the time you're sitting across from a bank, you already know where you stand.

2. Register as a First-Time Buyer with DLD

This is a step most renters don't know about. Dubai's First-Time Home Buyer Programme offers priority access to new launches, preferential pricing on off-plan units, flexible payment plans for DLD fees via eligible credit cards, and better mortgage rates from participating banks.

You register via the DLD website or the Dubai REST app.

Prosper's Relationship Manager handles this kind of guidance proactively, alerting you to programs, deadlines, and eligibility criteria before you think to ask. Rather than discovering the DLD First-Time Buyer Programme on your own, your RM flags it, walks you through the registration, and makes sure you're positioned to use your QR code to its full advantage.

3. Get Mortgage Pre-Approval

Pre-approval usually takes 2–7 business days and is valid for 60–90 days. It tells you exactly what you can spend, lets you act faster, and gives you stronger negotiating power with sellers.

Our premium mortgage partner, My Mortgage’s mortgage calculator simplifies your search by continuously monitoring interest rates and providing real-time recommendations based on your eligibility.

If you already have a mortgage on a rental property, Prosper can upload your details and suggest personalized refinancing options. Their mortgage advisors are also able to secure pre-approvals on off-plan properties — a step many buyers don't realize is possible.

4. Find the Right Property

Since Prosper already knows your rental history, preferred locations, lifestyle, and budget from your tenant profile, our Property Specialists don't have to start from scratch and can deliver tailored property recommendations immediately.

Through Prosper's strategic developer partnerships, you also get first-mover access to off-plan inventory before it hits the open market. The platform also shows you verified rental details for any property you're considering buying, so you know its investment income potential upfront — not after the fact.

5. Sign the MOU (Form F)

Once you agree on a price, both parties sign a Memorandum of Understanding (Form F). At this stage, a 10% deposit is typically required from the buyer. This is a legally binding document that protects both sides during the transaction.

Our Property Specialists will assist you throughout the documentation, advise you on compliances and make sure nothing is missed when filing the paperwork.

This is the same process Prosper handles for its landlord users when listing properties for sale, meaning the expertise is built into the platform. Your Relationship Manager stays in the loop, sending reminders and ensuring all paperwork is submitted correctly and on time.

6. Apply for Your Mortgage

With the MOU signed, you submit your full mortgage application. The bank conducts a full credit bureau check through the Al Etihad Credit Bureau (AECB) and carries out a valuation of the property before proceeding.

Prosper's secure document vault becomes critical here. All your identity documents, tenancy contracts, Ejari certificates, cheque history, and financial records are already stored in Prosper's encrypted vault, ready to be pulled instantly.

There's no scrambling for paperwork across emails and folders. My Mortgage advisors, working alongside your Relationship Manager, handle the bank liaison, track the application status, and flag any issues before they cause delays.

7. Get the NOC

For properties managed by developers, the seller must obtain a No Objection Certificate (NOC) from the developer before the sale can proceed.

Your Prosper Property Specialist coordinates this directly, liaising with the developer or building management on your behalf. It's one of the steps that frequently delays transactions when buyers go it alone, having a dedicated specialist who knows the process eliminates that risk entirely.

8. Transfer Ownership at the DLD

You submit your payment, original ID documents, NOC, and MOU to receive your title deed. Once you have the title deed, you're officially the property owner.

The DLD transfer fee is 4% of the property price.

After your title deed is issued, uploading it to Prosper instantly transforms your profile. You go from tenant to landlord on the platform, your new owner dashboard activates, showing your property's current ROI, 5-year ROI projections, performance benchmarking against similar properties in your area, and average rental income insights.

Everything you need to manage, monitor, or eventually grow your investment is ready the moment ownership transfers.

9. Own, Earn, and Grow

Properties worth AED 750,000 or more qualify buyers for a residency visa, and those valued at AED 2 million or more unlock eligibility for a 10-year Golden Visa. There's also zero property tax and no capital gains tax, making ownership in Dubai genuinely more advantageous than long-term renting.

Prosper doesn't stop being useful once you become an owner. If you choose to rent out your new property, Prosper manages the entire tenancy lifecycle, from listing and contract creation to tenant management and renewal alerts.

Eligibility Criteria for Rent-to-Own in Dubai

One of the key advantages of rent-to-own properties in Dubai is their relatively flexible entry requirements compared to traditional mortgage financing. However, you’ll still need to meet certain basic criteria before entering into an agreement:

1. Valid UAE Residency

Applicants must hold a valid UAE residency visa at the time of entering into a rent-to-own contract. This ensures that the agreement complies with local property regulations and registration requirements. Maintaining valid residency throughout the lease term is also important for a smooth transfer at the time of purchase.

2. Demonstrated Financial Stability

While rent-to-own plans are more flexible than bank mortgages, sellers and developers still require proof of consistent income. This may include salary certificates, bank statements, or employment contracts to confirm your ability to meet monthly payments. A stable financial profile reassures the owner that you can sustain payments over the full lease term.

3. Minimum Age Requirement

Most developers require applicants to be at least 21 years old to enter into a legally binding real estate contract. This aligns with standard property transaction regulations in Dubai. Some developers may apply additional criteria depending on the property type or contract structure.

4. Seller or Developer Approval

Final approval from the property owner or developer is mandatory before the agreement is executed. They will typically review your financial standing, employment status, and overall suitability as a long-term occupant. This approval process helps ensure both parties are aligned before committing to a multi-year arrangement.

Compared to traditional mortgages, rent-to-own agreements often involve fewer upfront financial hurdles. This makes them especially attractive for first-time buyers and professionals who are financially stable but not yet ready for a large lump-sum down payment.

Essential RERA Regulations for Rent-to-Own Contracts

Navigating the legalities of rent to own in Dubai requires more than just a handshake; it requires strict alignment with the Dubai Land Department (DLD) and the Real Estate Regulatory Agency (RERA).

RERA Compliance Overview

To protect your investment and ensure a smooth transition from tenant to owner, these are the non-negotiable legal pillars:

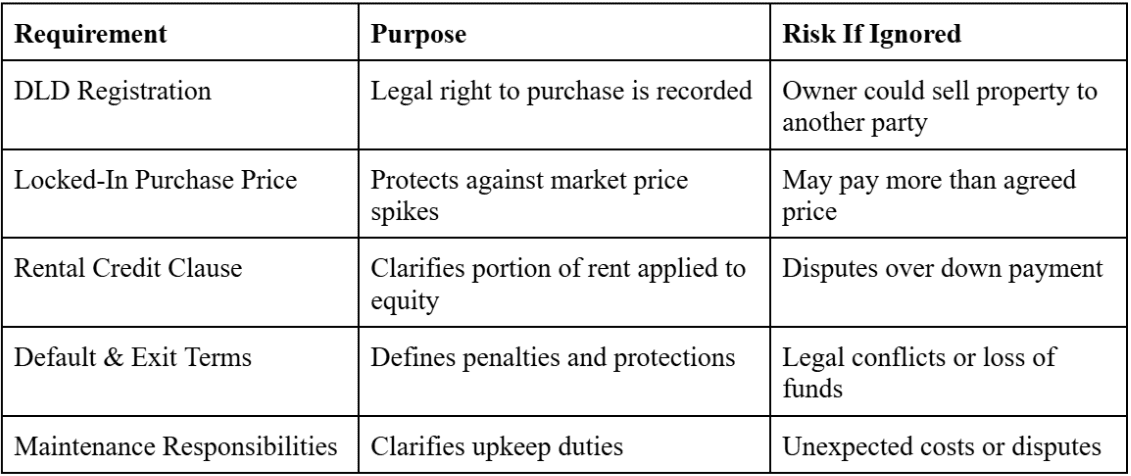

1. Official DLD Registration

Unlike a standard tenancy, a rent-to-own agreement must be registered under the DLD’s specific "Rent-to-Own" smart service. This registration is vital because it grants the tenant a legal "right to purchase" that is recorded against the property’s title deed, preventing the owner from selling to anyone else during your term.

2. Locked-In Purchase Price

RERA regulations dictate that the final purchase price must be clearly defined at the start of the contract. This protects those seeking rent to own apartments or villas in Dubai from sudden market spikes, ensuring that the price you pay in three or five years is based on the valuation agreed upon today.

3. The "Rental Credit" Clause

Your contract must explicitly state what percentage of your rent is a "rental payment" and what percentage is an "equity credit". For many rent to own properties in Dubai, this credit acts as your future down payment.

4. Clear Default & Exit Terms

RERA requires transparency regarding what happens if a tenant decides not to exercise their option or if a payment is missed. Generally, while you may forfeit your "option fee," the law ensures that your rights as a tenant remain protected under standard Ejari laws during the lease period.

5. Property Maintenance Responsibilities

Under RERA’s standard framework for rent to own in Dubai, maintenance responsibilities can differ from a normal lease. Often, the "aspirational buyer" takes on more responsibility for the unit's upkeep, as they are the future owner.

Popular Rent-to-Own Areas in Dubai

If the rent-to-own model feels like the right fit, choosing the right location is your next big decision. Dubai offers several well-planned communities where this structure is becoming increasingly available, particularly through reputable developers. Here are some of the most sought-after areas to explore:

- Dubai South: Dubai South is known for its modern developments, competitive pricing, and strong future infrastructure plans. Its long-term growth potential makes it attractive for buyers looking to build equity over time.

- Town Square: Town Square is popular for its affordability and vibrant, community-focused environment. With parks, retail outlets, and family-friendly amenities, it offers strong value for budget-conscious buyers.

- Mirdif: Known for its established suburban charm, Mirdif provides a quieter residential atmosphere while still offering convenient access to central Dubai. The area features spacious villas and low-rise developments, making it ideal for families seeking stability.

- Jumeirah Village Circle (JVC): JVC is a favorite among first-time buyers and investors due to its balanced mix of affordability and rental demand. The community offers a wide range of apartments and townhouses, making entry points more flexible.

- Mohammed Bin Rashid City (MBR City): The area features premium developments, luxury villas, and high-end apartments close to Downtown Dubai. Rent-to-own opportunities here can be ideal for those aiming to secure a high-value property over time.

Renting Vs Owning a Property in Dubai

The Benefits of Owning Over Renting

1. Your Money Works For You, Not Against You

This is the single most important financial distinction between renting and owning. Every month you pay rent, that money is gone with no asset created, no wealth built, no return. When renting, 100% of your payment is an expense.

With a mortgage, a significant portion builds personal wealth. Over time, that difference is staggering. A renter spending AED 90,000 a year over a decade has paid out AED 900,000 with absolutely nothing to show for it. An owner making comparable monthly payments is steadily accumulating an asset that belongs entirely to them, and that grows in value every year.

2. Protection From Dubai's Rising Rents

Rents in Dubai have witnessed increases of 20–30% year-over-year, driven by the city's expanding population and growing housing demand — leaving renters at the mercy of landlords and making long-term budgeting extremely difficult (Binghatti)

A fixed-rate mortgage eliminates this exposure entirely. Your monthly payment is locked in from day one. While a renter's costs spiral upward at every renewal cycle, an owner's mortgage payment stays exactly the same — and their property's value rises in parallel. The financial divergence between a renter and an owner widens significantly with every passing year in Dubai's market.

3. A Tax-Free Investment With World-Class Returns

Most countries penalize property gains heavily. Dubai doesn't. There is no property tax, no income tax, and no capital gains tax in Dubai — meaning a property that appreciates AED 500,000 in value puts the full AED 500,000 in your pocket upon sale, with zero tax erosion.

In markets like the UK, Australia, or the US, that same gain could be reduced by 20–40% through taxes. In Dubai, you keep every single dirham.

On top of capital appreciation, Dubai also offers some of the highest rental yields in the world — typically between 5% and 8%, if you choose to rent out your property. That's passive income flowing on an asset that's simultaneously growing in value.

4. Your Asset Appreciates While You Live In It

Villa prices in Dubai are up nearly 30% annually and apartment prices around 21% year-on-year by mid-2025 (Betterhomes) That capital appreciation happens passively — regardless of whether you're occupying the property or renting it out.

A property purchased today at AED 1.5 million doesn't stay at AED 1.5 million. In Dubai's current trajectory, it becomes a materially more valuable asset within just a few years, while your outstanding mortgage balance simultaneously decreases. The gap between what you owe and what the property is worth — your equity — grows from both ends at once.

Own a property in Dubai Seamlessly With Prosper

The path from renter to property owner in Dubai has never been more accessible — or more financially compelling. With mortgage rates at competitive prices, property values appreciating at record pace, and a tax-free environment that lets you keep every dirham of your gains, staying a renter is increasingly the more expensive long-term choice.

The question isn't really whether you can own property in Dubai. It's whether you have the right team guiding you through it.

That's exactly what Prosper is built for.

From analyzing your financial profile and connecting you with mortgage advisors, to assigning a dedicated Property Specialist and managing your investment long after the title deed is in your hands, Prosper turns one of life's biggest financial decisions into a structured, supported, and seamless journey.

Download Prosper today and take the first step from tenant to owner.