Dubai Real Estate: What the Market Is Really Telling Us Heading Into Summer

02/06/2026

|7 min read

As summer nears, Dubai's property market offers important clues. Learn what trends in prices and demand may signal next.

Dubai Real Estate: What the Market Is Really Telling Us Heading Into Summer

We are now five months into 2026. We have closely scrutinized and watched this market open with great momentum, soak up the ripples of a regional war, navigate a defiant ceasefire and still close every month with billions in residential transactions.

As we publish this in the first week of June, with summer officially kicking off and the city starting to exhibit signs of summer slow down, it is time to step back from the monthly commotion and assess what the full picture from January through April is actually telling us.

Because the picture is more layered than the headlines suggest. And if you are making decisions about Dubai property right now, whether it is to buy, sell, hold, or renew a lease, you deserve a full and transparent on ground story.

Four Months In: What The Trajectory Is Shaping Up Like

Before we get into what's to come next, here is what happened so far.

January was extremely promising. An estimated 16,305 transactions worth AED 53.6 billion, a very solid month on record, carrying 2025's consistent pace straight into the new year. Pricing held at an average AED 1,900 per sq. ft.

Buyer behaviour was more confident and intentional. Off-plan dominated at 71.5% of all residential transactions. The secondary market recorded over 5,000 estimated transactions with buyers focusing capital toward near handover units and substantial yield plays.

February confirmed the market was continuing at a steady level. Roughly 15,902 transactions worth AED 46.3 billion. Pricing remained steady at an approximate AED 2,000 per sq. ft. Buyers were less hypothetical in their approach and more pointed with their choices.

Developers with active construction projects and track records were absorbing demand faster than those that were in the initial phases of launch.

March brought the first real test. The Iran–Israel regional conflict escalated quickly, targeting Gulf infrastructure including UAE energy and transport assets. And even through this, around 12,978 transactions worth AED 37.2 billion were recorded. Average pricing remained at AED 1,900 per sq. ft.

Capital concentrated further into established developers and ready stock. The secondary market stayed active. The message from March was clear, this market was not waiting for the conflict to pass. It was adapting and operating through it.

April delivered a number that surprised; 13,335 transactions worth AED 38.5 billion which was up 2.8% from March in volume, despite the ceasefire of 8 April with both sides violating terms and the Strait of Hormuz under active naval pressure. Schools across the Emirates had shifted to remote learning. As we wrote in April's report: It will be remembered as the month Dubai's residential market transacted steadily through a war.

What Narrative The First Four Months Paint

Look at those four months as a whole and a crystal clear picture presents itself.

Transaction volumes settled into a single band. January's record high was always going to be the ceiling for a while. What followed after: 15,902, 12,978, 13,335 is not a sign of decline. It is a market finding its operational footing under genuinely rough tides.

Pricing barely fluctuated. AED 1,900 to AED 2,000 per sq. ft. across four consecutive months, through conflict and ceasefire and summer slow down. That is not a market cracking under price pressure. That is a market with deep underlying demand to hold its value while the world outside becomes more unpredictable.

Buyer behaviour changed. This is the shift that holds the most significance. In January, buyers were confident and more prone to risks. By March and April, they had become selective and measured. The same total capital was moving, the only difference was that it was into fewer, better-chosen assets. Projects with clear construction progress.

Developers with concrete delivery track records. Communities with authentic end-user demand, not just surface level appeal.

Off-plan remained dominant. Off-plan commanded roughly 77% of primary market transactions across this period. What changed is which off-plan? In January, buyers were broadly sure about the pipeline.

By April, under-construction resales had become the most cautious segment in the entire market for aspiring buyers, while off-plan projects from credible developers with visible sites continued to attract investment. The product is the same. The scrutiny is completely different.

Ready stock quietly gained strategic standing. Across all four months, completed assets have been gaining ground. Buyers are using ready property to barricade against construction risk, access immediate rental yield and maintain liquidity in an uncertain environment. This trend will only strengthen heading into summer.

The market that enters June 2026 is not the same market that opened January. It is a market changing its approach.

Here's What The Numbers Don't Show You

Here is something critical that the monthly headlines consistently miss.

A significant portion of what you are reading in DLD transaction data right now is not fresh demand. It is an old demand finally being registered.

In Dubai's property market, the gap between a sale being agreed and that sale materializing in DLD records can stretch to months. Off-plan units previously sold during the peak of 2024 and early 2025 are now crossing the DLD's construction completion threshold required for title deed registration.

They are surfacing in the updated data now, in Q2 2026, making today's volumes look more inflated than the present buying environment alone would otherwise showcase.

As data from April suggests, nearly 57,500 units have crossed that threshold and are lined up for delivery this year. By the end of April, an estimated 6,723 had already been handed over. By the time you read this in early June, that number is meaningfully higher.

The pipeline is in fact real. The construction progress is also very real. But these transactions represent commitments made in a different market momentum by buyers who made decisions before regional tensions came to light, before sentiment shifted, before the conversation shifted.

This is why reading April's approximate AED 38.5 billion figure as pure present-tense demand would not be accurate. Some of it is yesterday's conviction arriving late.

What Geopolitical Tension Actually Does To a Property Market

Dubai has never been insulated from what happens around it. The Iran conflict of early 2026 which led to missile strikes on UAE energy and transport assets, a turbulent ceasefire, the Strait of Hormuz under active naval pressure, has had real effects. Just not always where people expect to see them.

The most visible impact has been on sentiment and international buyer commitments towards the UAE. Investors who were on the brink of committing, paused. Airspace restrictions rattled arrivals.

Citi analysts revised Dubai's population growth forecasts from roughly 4% annually to around 1% for the entirety of 2026. For a city that thrives on its expatriates, cooled hiring across hospitality, energy and similar sectors is the signal worth watching closely.

In certain segments of the secondary market, property owners have been cutting asking prices to find buyers and garner more interest. The off-plan resale segment has felt the most of this stress, particularly investors who bought multiple units expecting to flip before completion and are now facing payment plan obligations without the buyer momentum they were used to having previously.

But hold that alongside the data:

What changed: International buyer flows have reasonably slowed. Some off-plan resale investors are under payment plan obligations. Population growth forecasts revised down from what was once anticipated. Certain sellers are pulling back on prices.

What didn't change: An estimated AED 38.5 billion still transacted in residential transactions in April which is still the on ground reality. Rental yields across leading communities remained between 7–9%. The government removed the minimum investment threshold for residency visas mid-conflict which is a direct, proactive response to sustain demand.

The Dubai 2040 Urban Master Plan. Zero income tax. A population that has already surpassed the 4 million threshold as of late October 2025.

For The Investor: Accuracy Beats Panic

The data and in turn the ability to tell the difference between performing and underperforming assets is very pointed today. That means both more risk and more opportunity, depending entirely on what you own or what you are buying based on your appetite.

What is holding: Renowned and well established communities with genuine lifestyle pull, proven infrastructure track record and limited new supply. Palm Jumeirah, Dubai Hills Estate, Downtown Dubai, Dubai Creek Harbour. End-user demand in these areas is concrete.

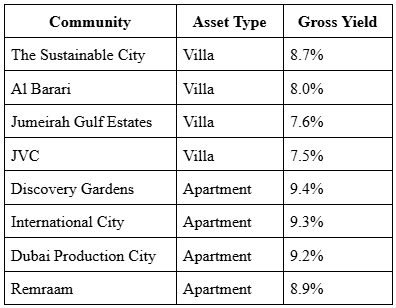

Average rental yields have remained consistent across all four months of data and the top 10 areas are as follows:

The question heading into summer is not "is Dubai safe?" It is: is my specific asset, in my specific community, positioned to weather what comes next? That is the data question everyone should be asking.

For The Homeowner: Your Equity Is Intact And Your Next Move Needs Clear Eyes

If you own a home in Dubai, you are in a strong position. Prices have not collapsed. Any movement has been minor and the present trend suggests it won't last that long. Pricing at approximately AED 2,000 per sq. ft. has been mostly stable across the entire January to April period.

What changes as we step into summer is the liquidity scenario. Fewer active buyers in June and July means your property takes longer to find the right buyer but that is the expected slow down with each summer. If you are thinking about selling, pricing your property to reflect today's market rather than peak 2025 is a reality you have to come to terms with.

If you are not selling, the picture is genuinely leaning more towards the positive side. The government's quick decision to remove the minimum investment threshold for residency visas is a direct policy signal clearly stating that the UAE is committed to sustaining this market's appeal and depth.

Your home is not just a property. In Dubai's framework, it is an anchor to a lifestyle and a residency pathway for an expat. One difficult quarter does not alter that equation.

For The Tenant: The Balance Is Shifting And It's Shifting At a Pace

The last two years have been difficult for renters to manage. Rental inflations were sharp, vacancy in desirable communities stayed tight for new entrants and renewal conversations often felt one sided.

With nearly 57,500 units nearing completion in 2026 and the handover pipeline accelerating into H2, rental supply is expected to increase over the coming months.

The summer slowdown, when vacancy naturally rises as residents travel and business activity softens, is expected to be more pronounced this year than in recent cycles. Some forecasters project rental prices in the low season declining by up to 5% in mid-market areas.

Prime locations and well-managed communities will retain their pricing. The luxury segment remains undersupplied. But in mid-market apartments, the segment where rental pressure has been most, tenants are sure to find more negotiating room between now and September than they have had since 2023.

If your lease is up for renewal in the coming months, use what the data suggests. What are comparable units in your community actually transacting at and not what they're just listed at? A landlord facing an August vacancy, with new handovers entering the market, has considerably more motivation to retain a good tenant than they will in October when the season switches.

What The "Summer Slowdown" Actually Means

The summer slowdown is real and also deeply misunderstood.

Transaction volumes in July and August are consistently lower than peak spring and autumn seasons as history suggests. It is simply a year on year calendar reality. Schools are closed, many residents travel and generally the heat keeps people indoors. International investors do not fly to Dubai during this time to tour properties.

But slow is not stopped. The market transacted at an estimated AED 38.5 billion in April through a war and that says something. It will transact through summer too, just differently.

What changes can we expect? New launch pace moderates, secondary market activity eases up, pricing conversations become more realistic on both sides.

What will stay? Authentic end-user demand, long-term investors with conviction and developers delivering against committed pipelines.

For investors with patience, summer is historically one of the better entry points in the Dubai cycle. Less competition, more motivated sellers and generally by October, when the season turns and the market accelerates, you are positioned rather than chasing.

Two Things To Watch Heading Into The Second Half

The Geopolitical Arc

A durable ceasefire, not the contested version seen in April, but one that genuinely reduces regional threat levels would certainly unlock a meaningful wave of deferred international buyer demand. Population growth and expatriate inflows are the most demand-sensitive variables in this market. Watch how they move.

The Handover Pipeline

With 57,500 units scheduled for 2026 delivery, the pace of actual completions will shape both rental supply and the resale market for off-plan inventory. Historically, 30–40% of projected pipeline slips into subsequent years due to a host of construction delays. If a meaningful portion of 2026 stock shifts to 2027, supply pressure eases naturally.

The Honest Picture Heading Into June

We started 2026 at AED 53.6 billion in January. We navigated a regional conflict, a turbulent ceasefire, schools going remote alongside airspace disruption. We closed April at AED 38.5 billion, up month-on-month by 2.8% from March.

That is quite a lot to go by and draw a fair assessment from.

What enters June 2026 is a market that has been tested in ways most markets never are and has demonstrated that its foundations are solid. At the same time, it is a market with genuine complexity that reveals a registration lag inflating near-term data, moderating international buyer flows and a summer season that will reveal more honestly than any other period which assets and developers have genuine substance.

That is exactly what we are here to help with with Prosper!

Data in this article draws directly on Prosper's monthly residential market reports for January through April 2026, sourced from Dubai Pulse (public government data) and REIDIN (licensed market data). All transaction figures are estimates subject to minor fluctuations. This article is for informational purposes only.